Positioning HSAs as a Must-Have Benefit

Webinar

Health savings accounts (HSAs) have become a critical component of a modern benefits package, yet many employees and even employers still don’t fully understand their long-term value.

In this session, Segal Benz Senior Communications Consultant, Jillian Roth, is joined by UMB Healthcare Services VP Marketing Manager, Mark Cordes, to discuss how we work together to craft compelling messages that drive employer adoption and increase employee engagement. They explore emerging trends in benefits communication, data-driven storytelling techniques, and best practices for positioning HSAs as an essential financial and health care tool.

In this webinar, you’ll learn about insightful strategies to:

- Craft a clear and compelling narrative.

- Leverage data to tell a powerful story.

- Address common misconceptions.

- Use current trends in communicating about HSAs and other benefits.

- Build a strong employer-provider partnership.

This webinar was previously recorded. View the full transcript below.

Transcript:

Ron Miller: Hello, and welcome to today's webcast, Positioning Health Savings Accounts as a Must-Have Benefit: Strategies for Employer and Employee Engagement. I'm Ron Miller, senior fellow at the Human Capital Center of The Conference Board, and I'll be your moderator for today's webcast.

Health savings accounts or HSAs have become a critical component of a modern benefits package, still many employees and even some employers don't fully understand their long-term value. In this webinar, Jillian Medoff of Segal Benz sat down with Mark Cordes of UMB Healthcare Services to discuss how they work together to help brokers and employers understand and promote the long-term value of HSAs by crafting compelling messages that drive employer adoption and increases employee engagement. They'll explore emerging trends in benefits communication, data-driven storytelling techniques, and best practices for positioning HSAs as an essential financial and healthcare tool.

There are five key takeaways for you today from this webcast. One, crafting a clear and compelling narrative. Number two, leveraging data to tell a powerful story. Number three, addressing common misconceptions, and the fourth takeaway, trends shaping benefits communication in 2025 and beyond, and finally, building a strong partnership.

So I'd like to introduce our two speakers today. Mark Cordes, the vice president, marketing manager, marketing communication of UMB Healthcare Services. Mark brings a history of marketing, design, and advertising experience, along with a passion for leveraging balanced right and left brain thinking to deliver innovative communication. He is responsible for the marketing and creative strategy, development and execution of UMB Healthcare Services brand communications, including all account holder communications and materials, employer and broker resources and communications, webinars, conferences, and sales team materials. UMB Financial Corporation is a financial services company headquartered in Kansas City, Missouri. As an established leader in the financial healthcare service industry, UMB brings a wealth of expertise to the full spectrum of benefit account administration.

Jillian Medoff, senior consultant with Segal Benz, has more than 25 years of experience developing communications initiatives for organizations of all sizes. She provides strategic counsel and hands-on support on a broad range of business issues across a variety of industries. Some of her clients include companies BMW, Nutanix, Exelixis, Salesforce, Shutterfly, and a few other companies I can't pronounce. Prior to joining Segal Benz, Jillian worked with Aon Hewitt and Deloitte Consulting.

Segal Benz is the communications consulting practice within Segal, the largest and oldest privately held employee benefits and HR consulting firm in the United States. Segal Benz provides trusted advice that improves lives and creates truly meaningful outcomes for their clients and their people. The organization serves a diverse group of clients, including leading large corporate employers, public sector organizations, and multi-employer benefit funds. One quick note on disclosures, I'll just let you read this for a few seconds and then I'll turn it over to Jillian. All right, Jillian, all yours.

Jillian Medoff: Thank you so much. Thank you for having us today. So today we're going to talk about HSAs and engagement. We'll start with looking at the current HSA landscape, and then we'll move to how to craft a clear and compelling narrative. Then we'll talk about ways to do that by leveraging data, communications, and measuring success. We'll then move to trends and communicating HSAs and other benefits, and building a strong client partnership. So I am going to turn the mic over to Mark who will take us through what's happening with HSAs currently.

Mark Cordes: Thank you, Jillian.

First, let's set the stage. HSAs have grown tremendously over the past decade, and they're now really a core part of many employers benefit programs and packages. Here's a quick snapshot right now where things stand. Between 2023 and the end of last year, HSAs had nearly $147 billion in assets across 39 million accounts. That's an almost 20% increase in just one year. Looking ahead, the HSA market is projected to continue to grow at this robust pace. By the end of 2026, Devenir projects that the HSA market will approach almost 44 million accounts with approximately 168 billion in assets. That's a pretty sizable amount. This is significant, especially with the increasing importance of HSAs in the benefits landscape.

But even with all that growth, there's still a fundamental gap in adoption and understanding of the HSAs. Plus, even when adoption is wrong, getting employers and employees to understand the full value of what that HSA offers can still be a challenge sometimes.

Most employers offer an HSA to their employees. In recent years, a survey of all those HSA sponsors with 500 employees or more, 84% offer HSAs and 83% make contributions to their employees accounts. However, only about 13% match employees contributions and only about 9% make that part of a reward or an incentive-based contribution, i.e., that you exercise, stop smoking, things of that nature.

So employees do or employers do understand how important seeding employees accounts is as a way to encourage engagement and participation. That said, however, in another study we find that only about 50% of employees were familiar with HSAs and only about 33% open new accounts. That's even when a company will offer to fund that. Furthermore, for several years the percentage of HSA account holders that make regular contributions has been fairly flat, hovering about 50% or so from about 2017 to 2021. That is, some of that was also due during the pandemic. However, recently this number has risen to an average of about 70%. While this is better, there's certainly room for improvement.

This gap in understanding about an HSA represents a missed opportunity. When employees and employers understand what HSAs really offer, and it's really this triple tax advantage as a way to pay for current healthcare expenses and also as a savings vehicle for retirement, that engagement and satisfaction can rise. When positioned correctly, they become really a game-changing part of the financial wellness program. We often like to say it's healthcare today, retirement tomorrow, because this is a financial device that you own. It is portable, you take it with you, it is yours. So it's really important that people understand that.

So the question is how do you reach brokers and employers and help them because they're the ones that in turn engage employees and communicate with their employees to understand what this is about because, let's admit, it is complicated, our healthcare system, and so this really is a very simple, straightforward, so how do you explain the power of that HSA. Also, how do you cut through all the noise to make sure your messages are heard? How can it be understood? How can it be easily acted upon? My tax advisor recently practically got up and gave me a hug because I was so passionate about the HSAs, and he has such a tough time getting some of his clients to understand what they can do with their HSA and how it is this great untapped financial planning tool. So Ron, I'll turn this first poll over to you.

Ron: Sure, Mark. And hey, it's pretty hard to get our tax advisors to give us a hug, so that's quite an accomplishment. So we'd like to take a quick poll of our participants, our audience, and ask you, within your organization, if you know what percent of the HSA account owners make regular contributions. If you could select the answer that applies to your organization, we'd appreciate it. I'll give you just about five to 10 seconds to do that. All right, I'm going to assume everybody's had a chance to answer the poll, and here are the answers, Mark.

Mark: Great, thank you. That kind of makes sense. I'm surprised there were in a few answers in the 25 to 50, but seeing that, it is difficult, and we'll talk a little bit about this in a bit on sometimes that has to do with, A, the company and what contributions they're making, but also in their workforce where they are. Is it a heavily younger workforce or an older one or a mix? That impacts this a lot, and at the end of the day it boils down to communication. So I think, Jillian, I'll pass I think this next one for you.

Jillian: Thank you. So the answer to both of the questions about how we cut through the noise and simplify is together Mark and I craft clear and compelling narratives that positions the HSA as a tool that supports both health and wealth. Most HSA marketing tends to lean heavily on the mechanics which is tax savings, contribution limits, and eligible expenses, but that kind of messaging doesn't exactly inspire action. So let's talk about how we get people's attention because you have to do that before you can get them to act. So here's one way, you can just tack on a popular character from a book, and my husband saw this slide and he was like, "Oh my god." So that's corporate humor. But one way we can do this in terms of getting messaging across is to reframe the story, and Mark just talked about this earlier which is instead of focusing on the math, we help show how HSA support employees' lives today and tomorrow.

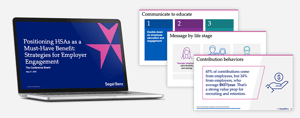

So to do that, we look at how they fit into an employee's worldview which is basically HSAs are a health and wealth tool, and we reframe the story to say healthcare now, savings later. In this way we're positioning HSAs as a health and wealth tool which is how the employees can capitalize on the HSAs primary benefits. So this positions the HSA as a unique tax advantaged account that allows employees to save on healthcare expenses now and at the same time build long-term savings for retirement. So this particular message, this is a webinar that we built for UMB, and it's called Healthcare Now, Retirement Later, The Power of an HSA. It's sticky, simple, and meaningful.

Moving a step further, storytelling really resonates when it's tailored to different life stages. We don't use a one-size-fits-all anymore when it comes to communication. Employees care about what's happening in their lives currently at this moment. Younger employees care about flexibility and savings, parents are focused on budgeting for family healthcare, and those nearing retirement are worried about Medicare costs. So we did a recent webinar where we hosted for brokers who are selling HSAs to employers, and we segmented messaging by life stage and provided sample communications for each group, and the feedback was overwhelmingly positive. They finally saw how to make HSA messaging feel personal and relevant, and part of that making that message resonate is backing it up with strong data. So, Mark, I'll let you speak to that after we do one more poll, Ron.

Ron: Okay. Well, we'd like to ask those of you on the webcast, within your company or your organization and in the past few years, have you noticed more employees contributing to their HSAs. All right, let's see what everyone has to say, and the answer's yes.

Mark: That's awesome. That tells me right there that I think there's a lot of folks on this call that are doing a pretty good job in communicating. If we saw a lot of no’s there, I think it'd be like, okay, we've got some more opportunities. But there's always more and more opportunities, and it's not even room for improvement, but just additional ways to help. So we'll talk about leveraging data and how to tell a strong story.

Contrary to your college class, data could be your friend. Whether it’s claims data, contribution patterns, demographics, these aren't just for reporting. These can really provide some insight, the pulse on what's happening, and can fuel incredibly effective storytelling. For example, the average funded HSA balance at the end of 2024 was about $4,700, but if you look at the accounts that are 15 years old, that average balance can often exceed 30,000. So there's a great little story here on long-term value and it helps to visualize this. And so this is something that could be used in speaking with younger or newer employees on how that slow and steady contribution can grow, and you can then say to your folks, "Look at what can happen in 10 years if you keep at this." That's a very tangible motivator.

On the employer side, contribution data is another compelling story. Last year, I thought 65% of HSA contributions came from employees and about 24% came from their employers. That averages about $927 a year per employee. That's a powerful value proposition. We have found consistently through the years, whenever employers fund their HSAs, it's not about that they're just giving them money. They're really investing in helping to support the long-term financial stability and security of that employee. That is a key message and driver for recruitment and retention, something that is a benefit that employers can really tout in their materials.

Jillian kind of mentioned this a bit ago, that we're using this data to segment our messaging, and that really helps in delivering the right message to the right person at the right time. If you're talking to a high-income employee, I think your message can leaner into the tax savings and investment growth opportunities. If somebody is just starting or they're really at a situation where they're living paycheck to paycheck, really can focus the HSA on how this can be their safety net, how this can help in an emergency when they have an out-of-pocket medical cost that they just were not planning for. So it's kind of that little extra bit of insurance. This is the same product, it's the same HSA, but different ways of looking at it and leveraging it. Of course, all of this needs to be communicated. It's really all about that. So, Jillian, let you take this.

Jillian: Thank you. I always like to start with one of my favorite topics around HSAs because we can have the best narrative and the strongest data, but if your employees still think that an HSA is used it or lose it, you're not going to get any traction. So there are five big myths that we encounter when it comes to HSAs. One is use it or lose it. Two, it's only for big emergencies. Three, an HSA is way too complicated to manage. Four, I have to use all the money in my HSA this year. Five, HSAs don't cover anything that I actually use.

So to counter these misconceptions, we recommend simple tools like a myth versus fact flyer. It might sound basic, but it makes a huge difference. You can highlight HSA basics, for instance, unlike FSAs, HSAs roll over indefinitely. You own the account, and HSA funds are portable. HSAs can be used for any emergency, however big or small. HSAs not that complicated, if you think about it in terms of tax advantages for paying healthcare now and then saving for retirement later. Your HSA is yours forever. HSAs cover many over-the-counter healthcare items. Here is just a snapshot of some of the things that HSAs cover. I'll just leave this up here for a minute.

So now we talk sometimes about investing. A lot of people don't realize that if your HSA reaches a certain number, then you can invest your balances. Employees and account holders who do invest tend to grow their accounts by five to 10 times more, and that's a massive educational opportunity. So we say sometimes think of it as a 401(k) for your healthcare and that clicks. Mark, I know you have a lot more to say about communications.

Mark: I do, and why we're talking that investment angle, you're right, and many providers, they will have managed funds for that investment that you could look at a particular timeline or your type of risk. You're right, it's a massive opportunity and it's really a great way to truly grow, and again, the money you put in, the money it grows, and the money takes out when applied to eligible items is all tax-free. So you're right. In my mind, education and communication are truly linked. Employers have this responsibility to educate, communicate, and offer guidance that will stay relevant to their employees as they continue their career and age.

So a number of things that you can do, double down on employee education, including regular communication about the advantages of saving versus spending, that power of compound interest that we keep speaking with, and that value of investing. Education and communication are probably the most important because they have a significant impact on employee engagement which in turn affects their productivity and retention. It's very expensive to bring in new employees. Take care of the ones that you do have. Focus on the HSA itself, the tax advantages, the timelines, the features as compared to FSAs and other financial tools, the flexibility of contributions and distributions and its role in individual retirement planning and also take advantage of policy shifts that support long-term saving, i.e., lower annual deductibles and out-of-pocket maximums, future legislation for generations of workers. For example, as part of those communications, letting your employees know that nowadays many retailers display right there if you're online ordering whether an item is HSA eligible. The legislation is frequently updating what is considered an HSA eligible item. Whether it's suntan lotion or CPAP supplies, that is constantly being expanded to meet the general population demands.

So that's not all. There’re still so many opportunities. Keep it going even after open enrollment, a cadence of year-round communications with employees who enrolled in the HSA plan as well as those who didn't engage. A great example that we've done with Jillian and Segal Benz is reminding account holders in Q1 communications that they can still make contributions for the prior year up until tax day that year. That's something that HSA account holders may not be aware of, but those are the things that position you as that employer in communicating and gaining that trust, respect, and source of knowledge for your employees. Your medical carrier and HSA administrator can help and with ideas about shopping for quality care, how to read the explanation of benefit statement, how an HSA fits into their long-term saving strategy, how to invest. All of these are messages that can be reinforcing and complementing each other rather than just be duplicated.

With any planned rollout, feedback is essential. Listen. Solicit reactions. Understand what your people are saying, and adjust your message, the education, the communications or plan accordingly and as necessary. Again, cannot stress enough the power of that consistent cadence and communication. It really can't be over-emphasized. In particular, really targeted communication that meets people where they are, when they are, and encourages them to take the next logical and attainable step. To create that momentum, it's really important to maintain that cadence.

A few more, approach savings as a holistic way of combining messaging around retirement savings and HSAs, ideally providing guidance on how to maximize both accounts. New employees or those that are new to the high-deductible healthcare plans, they might need a little extra guidance and education in how to understand that and how to track them into their optimal behaviors and maximize those benefits because their prior employer, that might not have been their benefit program.

As I mentioned earlier, navigating our healthcare system and all is complicated to say the least, but the high-deductible healthcare plans and the HSAs just kind of adds to it. However, they're pretty straightforward, and it's something that you can help prepare them so they can manage their program. A little ongoing support to help people get the most out of these resources will go a long, long way in people's understanding and in their view of that employer. And lastly, ensure your medical plan design supports having this, i.e., high-deductible healthcare plan along with attainable deductions, seed funding, and matching contributions which I know we've spoken a number of times here already. Jillian?

Jillian: Measuring?

Mark: Yes.

Jillian: Let's talk a little bit about communication measuring. So at Segal Benz, we work with employers and who in turn communicate with their employees. With UMB, we work with Mark to develop materials for employers, but also for brokers who then communicate with employer clients. So typically, you would measure success of your communications through ADHP adoption rates, increased enrollment in HSAs, and migration numbers. But in our case, since we don't have that insight, we measure webinar enrollment over the years which we have seen tremendous growth with more of the recent webinars we've done, certainly if they've been about the sticky messaging of healthcare now, retirement later, and when we look at HSAs in terms of where you are in your career, and we also look at post-webinar requests for information to see how effective the messaging we're doing is. So let's-

Ron: Hey, Jillian?

Jillian: Oh, go ahead.

Ron: I just wanted to mention to the audience, I'm seeing your questions come in and we are hoping to save some time at the end of this session to address your questions. So just be patient, we'll get to them, and if you have any further questions, add them in there. We'll do what we can to get to them.

Jillian: Thank you.

Ron: Thanks, Jillian.

Jillian: Sure. So let's shift gears a bit and talk about trends in communicating HSAs and other benefits and how we reach people through this messaging and materials. So digital first is the new normal. Mobile apps, text alerts, and video explainers have replaced a lot of traditional print materials, and it's going to go this way from now on. It's all about short, snackable content. When we do use print, it's for very important messaging and we don't do it frequently. We send materials to the home, but most of the materials we do now are digital. Here's one that we did for Synopsys which is, again, video. Personalization is everything, and we try to drill down to get as targeted as we can. In this particular example, we were tasked with encouraging HSA investing. So our message was people who invest their HSA money in stocks and bonds have an average balance of 14,000 compared with $2,500 for those who kept it a hundred percent in cash, and this kind of specificity and the suggestion of people like you outperform generic messages all the time.

We do multi-generational messaging. And so we understand that Gen Z responds to fast, casual content, boomers want retirement-focused information, and good communication respects those differences. Tailoring across groups is essential in our business. Here's another example of multi-generational marketing and messaging. In the past, you've seen where communication was really centered around open enrollment and once, maybe twice a year, and now we've really started doing education and communication year-round. So we do everything from 30-second explainers, one-topic emails, visual FAQs. Keep it stackable. We do drip communications, series, emails and series. A key part of your long-term financial planning, especially around HSAs, should be ongoing messaging 12 months a year.

Ron: And I think one of the keys, Jillian, is that your enrollment can change throughout the year.

Jillian: Mm-hmm.

Ron: You can change your level of participation. It's not a once-a-year decision that you have to make.

Jillian: Exactly. So every year brings new tools. Right now we're looking at AI strategies, so there's a lot more to come. We help employers’ future-proof their communication strategies. So, Mark, do you want to talk a little bit about how we maintain our relationship.

Mark: Certainly. Thank you.

As Jillian mentioned, none of this really works without a really strong employer-provider-consultant partnership. Although we work with a lot of employee groups, many of our clients are brokers and financial advisors, and they're not always communicating directly with those employees. That means their clients or employers need to carry these messages effectively. So that's where Segal Benz comes in. Together, we're collaborating with them to shape a cohesive strategy across the materials, whether it's one of the many webinars we do, our quarterly statements or emails, even one-off sheets, info sheets during open enrollment. All of these messages really reinforce the same key themes, and they're tailored to the audience. This is something that it's not one and done. This is not something that we just talk about once at the beginning of the year and off we go. We're staying in sync all year long to review what's working, what needs to be adjusted, what new strategies we want to test. That agility really helps us keep up with the changing employee needs and benefit trends.

We're constantly finding... if I see an interesting article or a report, we're constantly sending those back and forth to each other to really stay on top, and also seed ideas for, hmm, is this something that would help in one of our next communications. Over the year, we're working on these webinars, et cetera, and other time-sensitive marketing materials, and we really develop and shape that messaging to fit with the collateral at the right place at the right time, but it's always in this consistent voice, look, and feel. Like I mentioned, we're constantly in touch and we're really great partners because we both have a stake in investment in our mutual success.

So with that, I think, Jillian, if you don't have else, I think probably I'll start to wrap it up here, and I do see a fair number of questions coming in, so we'll get into those in a second, but I hope you're walking away from all this with a few key takeaways and ideas. One, craft a compelling narrative that speaks to both the head and the heart. It's not just about pushing a message. It's really about how to resonate with that audience. Use that data to create messages that resonate, that they're relevant. Help clarify and dispel these myths that create confusion and hold people back. Again, HSA, it's not use it or lose it. Keep it short, segmented, and ongoing. Make it sticky. Kind of what we talked earlier, it's healthcare today, retirement tomorrow. Finally, work with your partners and make sure the messages are consistent, clear, and actionable, and your different partners will have a little bit different feedback and insight into that. So with that, Jillian, did you have anything else to add or should we tackle a few of the Q&As here?

Jillian: I think we're done. I just wanted to say one thing that many client relationships don't last that long. I think the average is two or three years, and I just wanted to say that UMB and Segal Benz, we've been working together for like 14 years, and of those Mark and I have worked together for five. So we've seen a lot of changes, and it's been really, really, really satisfying for both of us. So that's all I really wanted to say, and we're happy to answer your questions.

Mark: Thank you. You guys have made it a very good, pleasurable, and productive relationship. Thank you.

Jillian: Thank you.

Ron: I have a question for you, Mark and Jillian. So if a company selects UMC Healthcare Services as their bank for HSA, do all your services come with that or do we pay extra for you and/or Jillian?

Mark: No, that is something, I work with Jillian, and we're providing that as part of our overall program. So we have quite the library of materials, not only for the employers but also that they can then give to their employees. We also have, I mean, it is literally hundreds of different pieces for whether it's a broker again or employer. We have a number of different presentations, webinars, documents. So it is full, so they don't have to go to... I'm working with Jillian and Segal Benz, and that's part of the package.

Ron: All right. Hey, Dirk asked a question. Once you become Medicare eligible and enroll in Medicare, you can no longer participate or contribute to an HSA. Are either of you aware of any efforts going on Capitol Hill to lobby for that to change so that Medicare participants can actually contribute to HSAs going forward?

Jillian: One of the things that has always been true of Washington is that HSAs and really retirement savings and retirement tools and programs are bipartisan, they're bipartisan issues, that everyone agrees that retirement is important, funding for retirement is important, and how do we help people become retirement ready. So I do think that there is always movement when it comes to change and progress around HSAs. At this point, I don't know if there's any specific dates when we can look forward to and say, "Oh yes, Medicare is going to be talked about and HSAs this year," but I do know that there are ongoing efforts all the time to make HSAs more available, more easily understood, and more successful for people in the long run.

Ron: Okay. Thanks. Anything to add, Mark?

Mark: No, I think Jillian said it well. I know our leadership, they're up on the hill annually in speaking with our representatives to help institute changes that will make it more beneficial to more Americans, whether that is broadening of who can have an HSA or the items that are HSA eligible. The wheels sometimes move very slow, but I know we are very engaged in that respect.

Ron: Good. How about the contribution limits? I don't recall, are they set to increase each year based on inflation, or how do the limits work today?

Mark: Funny enough, they were just... the updated from the IRS was announced a few weeks ago, and they're never enough I think sometimes for some folks, but we're updating that. So the 2026 numbers were just released. We're updating all of those materials right now as we speak.

Ron: Okay. All right. Melissa has a comment and questions to go with it. A big barrier to electing or switching to a HDHP with an HSA is not having the funds to cover the deductible expenses on the part of the employees. I have repeatedly seen earners go into... lower earners, lower wage earners go into high-deductible plans because of the low premium and low expectation of health issues, and they don't want to set aside more money on the HSA. On the other end, highly compensated employees who are in HDHPs are able to max out their HSA contributions each year, so naturally they find it a good strategy. Do you have any strategic recommendations for engaging lower wage earners in an HSA?

Jillian: That's a good question, and it does come up often.

Mark: Yes.

Jillian: I think the onus for employers is to explain how the tax benefits become advantageous if you contribute more, and it sounds paradoxical or counterintuitive, but the more you contribute, the lower your income, the income that you're reporting because you're getting the tax benefit of the contribution that you're making to your HSA. So in other words, if you contribute $75 instead of $50 every paycheck, the amount of reportable income is lowered. So it behooves employers to explain to their employees that you get benefits, you benefit from contributing more, even if it feels like your paycheck is going to shrink, but you're actually going to pay less taxes on what you're taking home.

Ron: It's kind of the same discussion as the 401(k) conversation, right?

Jillian: Right.

Ron: If you're going to contribute a hundred dollars a paycheck to your 401(k), or in this case your HSA, your net income effect might only be $80 or $85 because of the tax savings that you have on it. So it's a very similar discussion I think as with the 401(k), and Mark, you were going to add to that.

Mark: No, this is a subject that Jillian and I have spoken about many times over the years. It's I won't say a running joke, but whoever called it a high-deductible healthcare plan I think should be in the marketing hall of shame. It's really, it's a low premium healthcare plan. Another angle to look at it, especially if you think that you might have some upcoming expenses, putting aside that money and in front of that expense is almost like thinking about it, that tax break really, you could think about it as a discount on what that is going to cost down the road. I don't want to just, it's not like a coupon or anything, but if you know you're going to have to spend a thousand bucks on whatever, hip work-

Jillian: Braces.

Mark: ... braces, taking that money and putting that in HSA today, a year from now than when you go to use that it is almost like getting a 20 to 30% break on that expense. So there're different ways to look at it, and that's where working with Jillian and her team, you can build that narrative and make it compelling and put it in a way that is not policy wonkish, but it is more consumer friendly and understandable.

Jillian: It's almost like more in your... HSAs give you more in your paycheck as well as more in your savings account because you're saving the money for later for braces, but at the same time you're getting a tax benefit so your paycheck isn't hit as hard as you might think. It's daunting to think, "Oh, I'm going to save another a hundred dollars toward my HSA." That hundred dollars feels daunting because it's coming out of your paycheck, but in fact your paycheck, it's not hit as much because you're getting a tax break. I think that's a hard message to... it's a hard message to understand unless it's broken down in easy-to-understand language.

Ron: I have two more questions, and I think I'll read them both because they might overlap. Nobbit is asking, "How do you position HDHPs with HSAs as beneficial on a day-to-day basis?" And Liz asked, "Oh, by the way, how about how do you reach populations in hourly production sites, and what considerations do you have for communication overload?" So I wonder if those two questions relate. How do you position on a day-to-day but without overloading people? And while you're at it, how about folks that might not be at a desk every day and they're on a production line?

Jillian: One of the ways that we've really started communicating certainly with hourly workers is through text messaging and Slack messaging and Teams messaging. The phone is such a powerful tool and everyone has one that if you can create campaigns that are viewable on a phone that come in similarly like texts, you can create messaging around HSAs that people will see even if they're not at a computer or a desktop. I think when it comes to day-to-day messaging, there's the power of imagery versus words, and I think seeing images and doing that on a regular basis, I think that is a way to maintain a connection and engagement.

Ron: But if you're getting daily messages, how do you manage the overload? Or if I go back to your slide that showed a plan which I think is really useful, a plan for communication outreach each month of the year, how do you know if you're overloading them and they just basically start ignoring you instead?

Jillian: Well, I don't know that we would do daily texting, but we would, over the course of a twelve-month program we might incorporate a lot of different types of media. We would do everything from video to email to text to Slack to Teams, and then one, usually one big mailer to the home. So it's an ongoing series of interconnected but comprehensive communications that are visual, everything is interconnected. So we're trying to touch all five senses with different media.

One of the things that we do is we'll create an editorial calendar for the course of the year, and it'll include everything from Facebook messaging to text to emails, brochures, flyers so that it's holistic, but that you're getting a different look and message each time. So you're not realizing... you're getting messages that all are part of the same campaign, but everyone is different, so you're getting a different angle on the same type of tool. For instance, if it's an HSA, we'll talk about tax savings in the beginning of the year, and then as the year goes on we'll look at all the different ways that an HSA helps your life at different parts of the year and the different benefits that it has.

Ron: You glanced over a term earlier that you said, snackable, make them snackable. I think that's one of the key features too I believe, right? You want to elaborate on that a little bit?

Jillian: I think that consumers now are very used to short, quick, sweet, and impactful messaging, and by that I mean we refer back to healthcare now, retirement later. It's quick, it's easy, it's a snack, it's not a full meal, but at the same time it says a lot. The HSA is designed for tax benefits now and on reducing your healthcare expenses, but long-term financial stability. The quicker and easier and more digestible you can make the messaging, the better off you are in the long run.

Ron: Beautiful. I have one more question, I'll throw this one at you, Mark. Dirk mentions that Fidelity says that in retirement you'll need $150,000 just to pay for your out-of-pocket medical expenses. Now if you draw from your 401(k) to pay for those, you'll get taxed, whereas on an HSA you won't. Maybe you can comment on the triple tax impact that was on one of your slides earlier.

Mark: Certainly, and actually that one's kind of a bit of a low estimate. Some recent numbers that we have seen actually are closer to 300 to 350,000 that the average person will need in retirement to cover out-of-pocket medical expenses. So it is, it's a daunting proposition and something that one wants to think about as early in their career.

But as far as the triple tax advantage, it's the money that is going in each pay period, paycheck, month into your HSA is not taxed. The growth of those funds over time is not taxed, and when the funds are taken out to pay for eligible expenses, they are not taxed. So no, you can't go and buy a fishing boat or a jet ski, but the list of eligible expenses grows and grows, and I think you'd be hard-pressed to not find quite a few things there that are expenses that you'll have later in life. But it also covers things as basic as, as I mentioned, sunscreen. If you need orthotics, if you need your Theragun for a massage, all of that is covered. Feminine products were added a few years ago. So it's a pretty broad list.

Building off of what Jillian just said, communicating all of this, you're coming at it at different angles. Think about it, it's almost like episodes in a full story and you're looking at it from these different angles, and so there is a sweet spot of that cadence. You don't want to over-communicate, but it's also not just a once a year at open enrollment either. So it's just that slow, steady, focused, digestible, memorable communication that's key.

Ron: That completes the questions that have been submitted by the audience. We have a few minutes left to close. I think we'll go ahead and do that at this time. Jillian and Mark, thank you so much for today.

Jillian: Thank you, Ron.

Mark: Thank you, Ron.

Jillian: If you guys want to take a scan of this code here, you can get more information on Segal Benz, and if you'd like to reach out directly to Jillian, here's her email address, and once again I'll say thank you.

I have just a few slides to go through from The Conference Board to wrap up. There are other webcasts coming up if the audience has some interest in these. You can see Leading Through Uncertainty, very timely topic, How the Private Sector Can Protect Employee Well-Being, and How to Navigate a Reimagined Workplace in 2025. There's also a CHRO networking group if you have any interest. There's a QR code there that you can scan for that. And you might be interested in the trusted insights that come from Steve Odland, the president and CEO of The Conference Board, and you can scan again that QR code to get to those. And then for members of The Conference Board centers or councils, There's Trusted Insight for What's Ahead app that can be downloaded. myTCB is a member site that people can get a lot of information that's coming from The Conference Board research.

There is a summit in the month of June for CHROs. If you are a CHRO or if you have one who might be interested, please pass that on to them. Every single slide has a QR code here. What did we used to do when there wasn't QR codes? Can't even remember. So anyway, there's a few upcoming events, conferences that'll be held in Brooklyn, New York, various topics that you might be interested in. And I think that is a wrap for today. Again, Mark and Jillian, thank you so much.

Thank you, Ron.

Ron: We do have two minutes left if you have any final comments that you'd like to make.

Jillian: No, it was great. Thank you so much for having us, and I'm certainly happy to talk to anyone about communications at any time.

Ron: Thank you for dialing in, everybody.